The rising risks in being an agent

The ever-evolving risks affecting the property industry are easily overlooked by a busy agent under pressure, says insurance expert Oliver Wharmby. Here’s a timely reminder.

Charlie Bending, partner at DAC Beachcroft LLP, who specialises in defending claims against property professionals lays out the threat: “In addition to lender claims against valuers, particularly by short-term lenders, we do anticipate claims by aggrieved landlords against property managers increasing over the next 6-24 months; these are likely to flow from rental default caused by anything from a failure by the property manager to take steps on behalf of the landlord to address maintenance issues to (more likely) tenants being unable to pay or refusing to pay rent, due to their adverse financial situation.

We do anticipate claims by aggrieved landlords against property managers increasing.”

“Having protection from eviction [residential] or protection from forfeiture [business] due to the Coronavirus Act 2020 will only increase landlords’ losses, potentially leading to claims that the property manager failed to vet tenants appropriately. Once the protection ends, property managers will also need to have the capacity to act swiftly in order to kick-start the process; taking care to adhere to time limits and prescribed steps to avoid making a potential bad situation worse.”

Claims and new threats

There is no doubt we live in a society where there is an ever-increasing claims culture.

Extensive choice coupled with advanced technology, social media, online claim centres, chat rooms, blogging, No Win No Fee law firms have all served to educate the consumer of their rights who in turn have become increasingly demanding and litigious.

With the use of online platforms and the wide variety of communication mediums available, maintaining customer service levels has become increasingly challenging. The Property Ombudsman recorded a 20 per cent increase in complaints for 2019 and over last two years has seen a 250 per cent increase in customer service-related tweets on Twitter; sixty per cent of consumers will expect a response back within the hour.

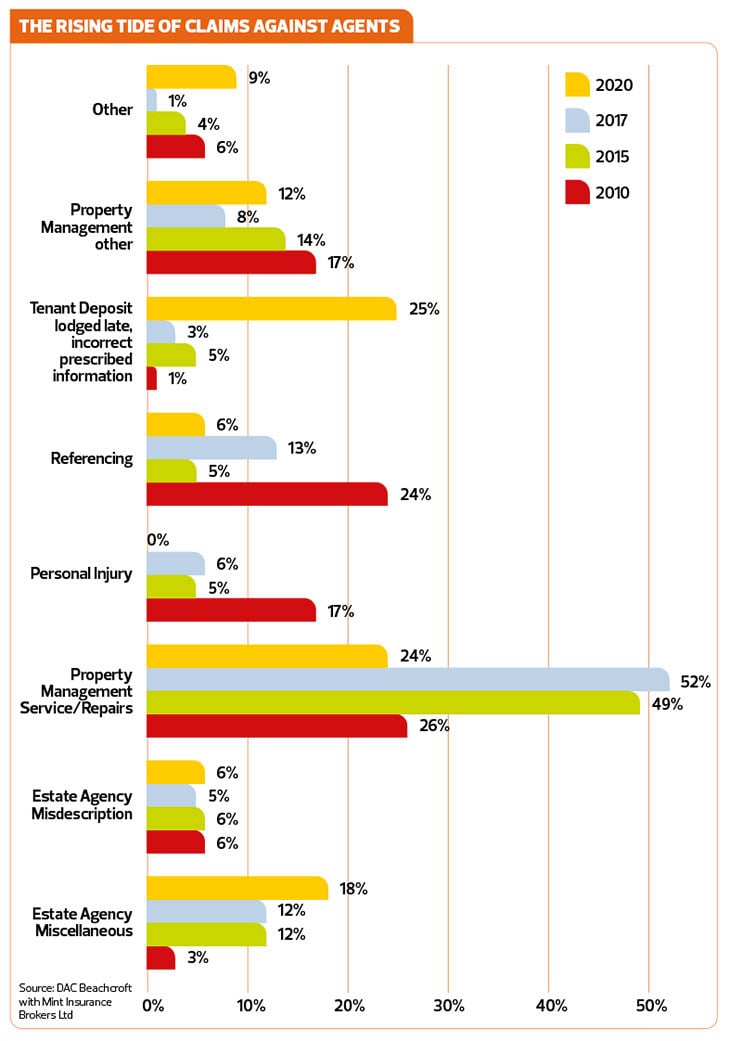

The rising tide of claims against agents

Property management claims continue to show consistent frequency, however the most notable development in the last 18 months comes from the surge in claims due to tenant deposits not being lodged on time and prescribed information being issued incorrectly.

It has been well documented that the courts can award up to three times the value of the deposit where a deposit has not been lodged on time, therefore tenants are being much more attentive and especially if prompted by a No Win No Fee law firm.

We have seen a marked increase in employee fraud and dishonesty claims since 2020 and mainly through client money misappropriation. Due to the volume of claims proportionate to claims under other categories being low, there is no allocated category for fraud and dishonesty, however you can see on the ‘other’ category how the frequency has increased from one to nine per cent. This also includes a rise in DSS discrimination claims building momentum following recent success.

Cyber crime

The chart does not include cyber claims as cyber liability is not typically included under a PI policy, however it is important to note the increasing threat of cyber liability and especially now GDPR has come in to force. During the pandemic, data from Interpol shows that ransomware incidents have increased by more than a third and Phishing/Scam/Fraud claims have increased by 59 per cent.

This has triggered a substantial correction in cyber insurance premium rates being charged and insurers are asking for more data and demanding much tighter risk management procedures.

- Europol – the government agency responsible for monitoring crime across Europe announced that cyber-crime was the biggest threat facing computer users.

- The PwC’s Global Economic Crime Survey (GECS) revealed that cybercrime is now the most common type of fraud for businesses in the UK.

- Up to 88 per cent of UK companies have suffered breaches in the last 12 months.

- One small business in the UK is successfully hacked every 19 seconds. Around 65,000 attempts to hack small- to medium-sized businesses (SMBs) occur in the UK every day, around 4,500 of which are successful. That equates to around 1.6 million of the 5.7 million SMBs in the UK per year.

CYBER CRIME DEFENCE CHECKLIST

Regular password updates on all devices.

Password complexity – Strict password rules should be implemented. Keep variety eg different passwords for different accounts.

- Do not share your password.

- Two Factor Authentication where appropriate.

- Staff training to be aware of phishing emails and the damage they represent. One in every 3,722 emails in the UK is a phishing attempt. Around half of cyber attacks in the UK involve phishing

- Software updates.

- Ensure files are encrypted.

- Monitoring of mobile and home working procedures.

- Never, under any circumstances, should a payment be made to a new bank account without verbal confirmation that the account details are genuine.

- Cyber Liability Insurance.

Cyber sophistication

Cyber criminals are becoming increasingly sophisticated and would appear to have switched their attention from large corporates to SME’s. The reason being SME’s are, typically, more vulnerable with weaker defences which make it easier for the hacker to penetrate IT systems.

We recommend your cyber policy includes social engineering claims, cyber-crime cover, business interruption, instant response cover and brand reputational damage protection.

Risk management guidance

Consumer protection is important and should be encouraged, however we are seeing an increasingly worrying trend where claimants are pursuing agents regardless of whether there is any substance to the claim, in the hope insurers shall settle. Typically, the claim values are low eg £2,500 – £5,000 where going to court would cost the insurers more in defence costs therefore they settle out of court.

Oliver Wharmby is a Director at Mint Insurance Brokers, servicing the insurance needs of property professionals.