What goes up…

House prices continue to rocket skywards, but with war in Europe and inflation and interest rate on the rise, it can't last, as Kate Faulkner of Designs on Property reports.

Headlines

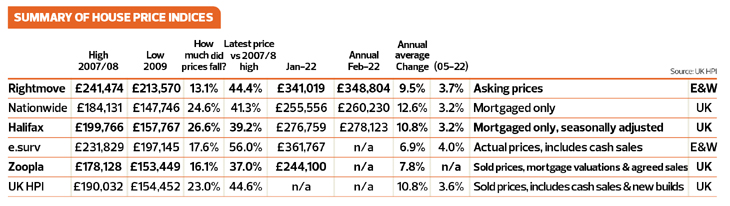

Rightmove

Biggest ever monthly price jump sets new record high as movers fear missing out

“Price of property coming to market rises by 2.3% this month (+£7,785) to a record of £348,804, the biggest monthly jump in pounds recorded by Rightmove in more than twenty years. Prices are now 9.5% higher than a year ago, the highest annual rate of growth since September 2014.”

There does appear to be more stock coming through, according to Rightmove…

RICS

Pick-up in new buyer enquiries supporting near-term sales expectations

“New buyer demand rises over the month.”

Nationwide

House price growth accelerated in February, with average price up £29,000 over the last year

“Annual house price growth accelerated to 12.6% in February, up from 11.2% in January and the strongest pace since June last year. Prices rose by 1.7% month-on-month, after taking account of seasonal effects, the seventh consecutive monthly increase.”

Halifax

House prices rise at fastest annual pace since 2007 to reach new record high

“Monthly house price growth rose to +0.5% following a slower start to the year. Annual rate of growth at +10.8% is the strongest level since June 2007 (+11.9%).”

E.surv

South East of England leads the way after nearly 14 years

“England and Wales monthly and annual growth edging down at 6.9%.”

Zoopla

UK house price inflation at +7.8%

“Average UK house prices rose by 0.9% in the three months to January, taking the rate of annual growth to 7.8%, down from 8% in December. Price growth gained momentum during most of 2021, after one of the busiest years the market had ever experienced. But with the lowest level of quarterly house price growth since August 2020, there are signs now that price growth is starting to ease, although the path will not be linear.”

Kate says: We should view some of the property prices this month with a bit of caution as there are suggestions from the likes of Zoopla that the market is slowing, while most indices are still suggesting price rises are on the increase. That’s not bad news, it has to happen, and we should remember that many areas across the UK haven’t done that great during the pandemic, including parts of London and even as far as Aberdeen. We have so much better data available from individual property price changes going back as far as 2000, through to property type and by postcode, it’s really this information that everyone should be focused on, particularly when working with individual buyers and sellers.

Kate says: We should view some of the property prices this month with a bit of caution as there are suggestions from the likes of Zoopla that the market is slowing, while most indices are still suggesting price rises are on the increase. That’s not bad news, it has to happen, and we should remember that many areas across the UK haven’t done that great during the pandemic, including parts of London and even as far as Aberdeen. We have so much better data available from individual property price changes going back as far as 2000, through to property type and by postcode, it’s really this information that everyone should be focused on, particularly when working with individual buyers and sellers.

There are suggestions from the likes of Zoopla that the market is slowing, while most indices are still suggesting price rises are on the increase. That’s not bad news, it has to happen…

House price growth by region in England

Kate says: Another factor that many of the ‘doomsday’ theorists are ignoring and why I think they may be proved wrong (or it could be me!) are that property prices in previous bubbles have gone up everywhere – and all prices have risen. Looking at today’s data though, that isn’t the case to date. House prices have risen in many places, but flat prices are just that, flat as a panic for many buyers and owners.

The more 2022 continues, the more I think property prices are going to be extremely dependent on the individual supply and demand for that property at the time it comes up for sale. This is tough for the media to get across to buyers/sellers, but it’s essential for agents in particular to do so. Using the average results from the stats we have seen to date rather than an agent’s local knowledge is essential for buyers to listen to. I’m also not a great fan of the automatic valuations often used to drive leads as when the data is like this, it could end up under-pricing some and overpricing others – and we know how badly that ends for everyone!

For me, pricing a property for market is an essential skill only a good agent has, while a surveyor takes this knowledge, looks further at the data and considers the property’s value, bearing in mind the condition and other factors that they would take into account.

RICS

“Respondents across all parts of the UK continue to report a further uplift in prices, with the North West and South East of England now seeing especially sharp rates of growth.”

Halifax

“Seven UK areas are now seeing double-digit annual house price inflation, highlighting not only the strength but the breadth of gains across the country. Wales was once again the strongest performing nation or region, with annual house price growth of 13.8%, largely unchanged since January. The South West of England also continues to record big gains. Annual house price inflation is now up to 13.4%, with by far the strongest quarterly growth (3.5%) of any region. While there will be a variety of local factors influencing the strength of these respective housing markets, it’s notable that both areas benefit from greater availability of more rural, scenic living which has proven to be so popular amongst buyers throughout the pandemic.

“Elsewhere, Northern Ireland also continues to record strong price growth, with prices up 13.1% on this time last year. House price growth remains robust in Scotland too. That said, despite the annual rate of house price growth picking up to 9.2%, remarkably Scotland now has the ‘weakest’ rate of annual growth of any area outside of London, again testament to the strength of house prices right across the UK. As indicated above London remains the weakest performing area of the UK, though the capital continued its recent upward trend with annual house price inflation now standing at 5.4%, its strongest level since the end of 2020.”

E.surv

“Four areas have seen an increase in their annual rate of growth, while six saw a fall. The four areas with an increase in rates are, in reverse order, Yorkshire and the Humber up 0.5% to 5.3%, the South West up 1.2% to 7.2%, Greater London up 2.1% to 8.0% and the South East up 1.9% to 11.7%. The South East is now in top position in the league table, after being absent for more than a decade, with the West Midlands falling to third place – having been in top place last month. This is the first time that both Greater London and the South East have been included in the top four areas of house price growth since August 2020. Demand for properties after this date had tended to be outside of the south east corner of England, as lifestyle changes brought about by the pandemic tended to favour scenic open spaces in more rural areas or in coastal locations.”

Property transactions, demand and supply

Kate says: Currently I’m getting very different feedback from the market. Some are saying it’s as busy as it has been for the last few years, while others are definitely seeing a slowdown, but, as with prices, it’s very localised. The good news is for the market is that there does appear to be more stock coming through. According to Rightmove, there are 11% more property listings than last year, while Zoopla data is seeing more stock come onto the market in most regions this year versus last.

Zoopla

New supply of homes for sale gathering momentum

“The imbalance between buyer demand and supply is not going to unwind in the near term. In late February, buyer demand for homes was 70% above the five-year average, and the total stock of homes available for sale was 43% lower.

“However, the recovery in the levels of new supply is gathering momentum. In January and February, new listings were up in every part of the country compared to 2021 as more movers, and landlords, listed their homes for sale.”

“The UK was in lockdown in early 2021, which means the annual comparison is flattering. But what is also telling from the chart above is the relationship between listings early this year and the longer-term trend before the pandemic.

“In several regions, including Scotland, the East Midlands, the North East and Yorkshire and the Humber, new listings over the last two months exceeded levels seen in 2017-2020 over the same period, signalling a turnaround in supply. New listings were broadly in line with longer-term trends in the North West and the West Midlands.

In the South West and Wales, where there are larger disparities in listings numbers in January and February compared to before the pandemic, home values are seeing the biggest annual rises, with higher levels of demand and that lack of supply pushing up pricing.

“When it comes to the type of properties being listed, there will be welcome news for markets with high concentrations of families moving, as there has been an annual rise of more than 10% in new listings for larger three and four-bed detached homes. In fact, new supply across all of the most common property types have risen year on year, meaning more listings in the last two months than in the same period in 2021.”

Rightmove

“There are signs that both buyers and sellers fear missing out in the current competitive market:

- More potential buyers are sending enquiries to agents, with the number 16% higher than this time last year

- New property listings are up 11% compared to the same period last year, suggesting more sellers are coming to market before looking for a property to purchase, to avoid missing out on their next home

- The number of people requesting a home valuation from an estate agent was up

- London records biggest annual jump in number of buyers sending enquiries of any region, and highest annual rate of price growth since 2016, as the end of pandemic restrictions and a return to the office fuel renewed demand in the Capital.”

RICS

“With respect to new buyer demand, +16% of respondents cited an increase in enquiries during January. This is up from +9% in December and, although only modestly positive, represents the strongest figure since May 2021. At the same time, the survey’s indicator capturing new instructions remained in negative territory. Meanwhile, sales volumes were more or less steady during January, having weakened to some degree throughout much of the second half of 2021. It is also worth noting that the average time to finalise a sale (from initial listing to completion) has steadily fallen over recent months, from an average of 17 weeks in the September survey to 16 weeks in January 2022.”

Halifax

“Lack of supply continues to underpin rising house prices, with recent industry surveys showing a dearth of new properties being listed, now a long-term trend.”

NAEA Propertymark

“The average number of sales agreed per member branch rose slightly to seven in January, from five in December. This is 40 per cent more than December 2021 and reverses the trend of decreases in the final three months of last year, although it is down 30 per cent on January 2021’s figure of ten. Purchases by first-time buyers made up 29 per cent of sales in January – a 26 per cent increase when compared to January 2021.”

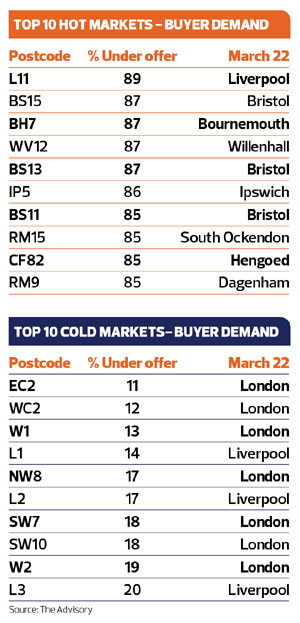

Postcodes – hot or not?

The Advisory track current market conditions so buyers and sellers can gain an independent view of how easy it would be to buy and sell their home in their area. This makes it easier for good agents that are honest about market conditions to value and manage expectations. For example, in L11 (Liverpool) 89% of the properties on the market are under offer and EC2 in London is one of the worst performers according to this index, showing that ‘average property prices’ can mislead buyers and sellers.

From PropCast’s perspective, the hot markets at postcode level don’t necessarily track the overall increases and decreases seen even at town and city levels, with Liverpool, Bristol and Bournemouth having some of the busiest markets, and London and L1, L2 and L3 Liverpool having some of the slower ones.

To find out what’s happening in your postcode visit the House Selling Weather Forecast.