CITY TRACKER: Inner and outer London property joins North-South divide

Kate Faulkner provides her latest house price update by town and city, highlighting the emerging divide between inner and outer London property.

Our City Tracker shows that although there is a North-South divide, there are also differences with regions too, including the London property market.

Our City Tracker shows that although there is a North-South divide, there are also differences with regions too, including the London property market.

For example, Wales is doing well year-on-year in most indices, but looking at Cardiff, prices are still lower than they were in 2022 – although only just! And in London, data from E.surv shows that, while average prices are down by 3.6% year-on-year, this is mostly being driven by falls in the higher-value inner boroughs.

![]()

We still have 17 out of our 30 Cities still to recover to 2022 prices – and of course that doesn’t include how far they are behind from an investment perspective due to inflation rising by 16% during this period. And, a similar number of cities are seeing property prices rising at a lower rate than inflation.

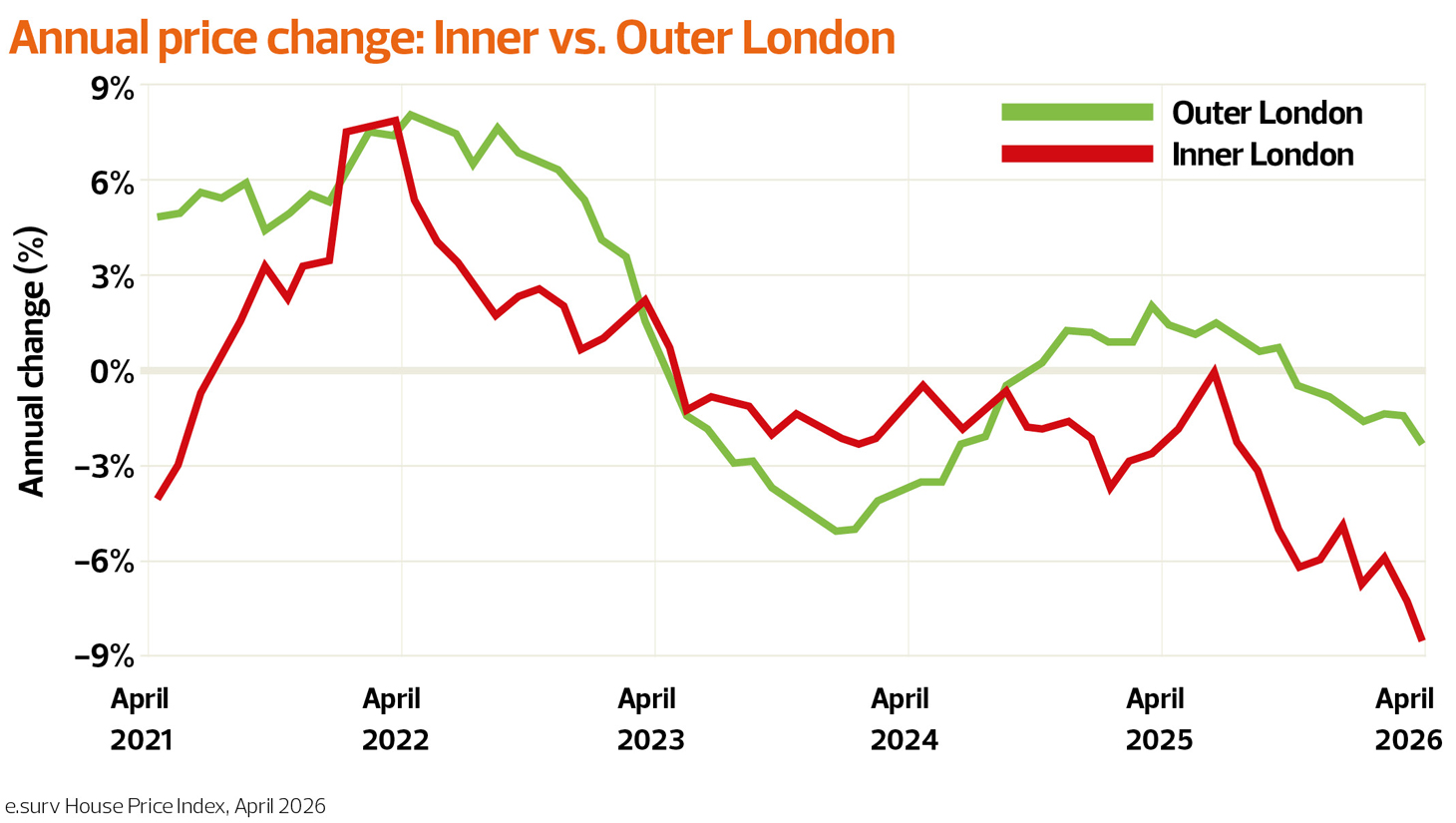

E.surv have done some great analysis on the London market, comparing inner and outer London.

“Inner London prices are down 8.7% year on year, compared with a 2.6% fall in outer London. The average inner London price is £687,415, compared with £518,655 in outer London — a gap of almost £169,000. The most expensive parts of the capital are seeing the sharpest falls, while outer London is weakening by much less.

“Outer London continued to show annual price growth through much of 2024 and early 2025, while inner London had already started to register price falls. Those falls have become sharper over the past year, suggesting the pressure in London started in the higher-value inner boroughs before spreading more widely.

“Outer London is softer than a year ago, but the sharper fall is in inner boroughs. Higher values leave buyers more exposed to affordability pressure, while tax changes are likely to weigh most heavily on the top end of the market. The composition of the market also matters: inner London has a larger flat sector, and flats have been one of the weakest parts of the capital’s housing market.”

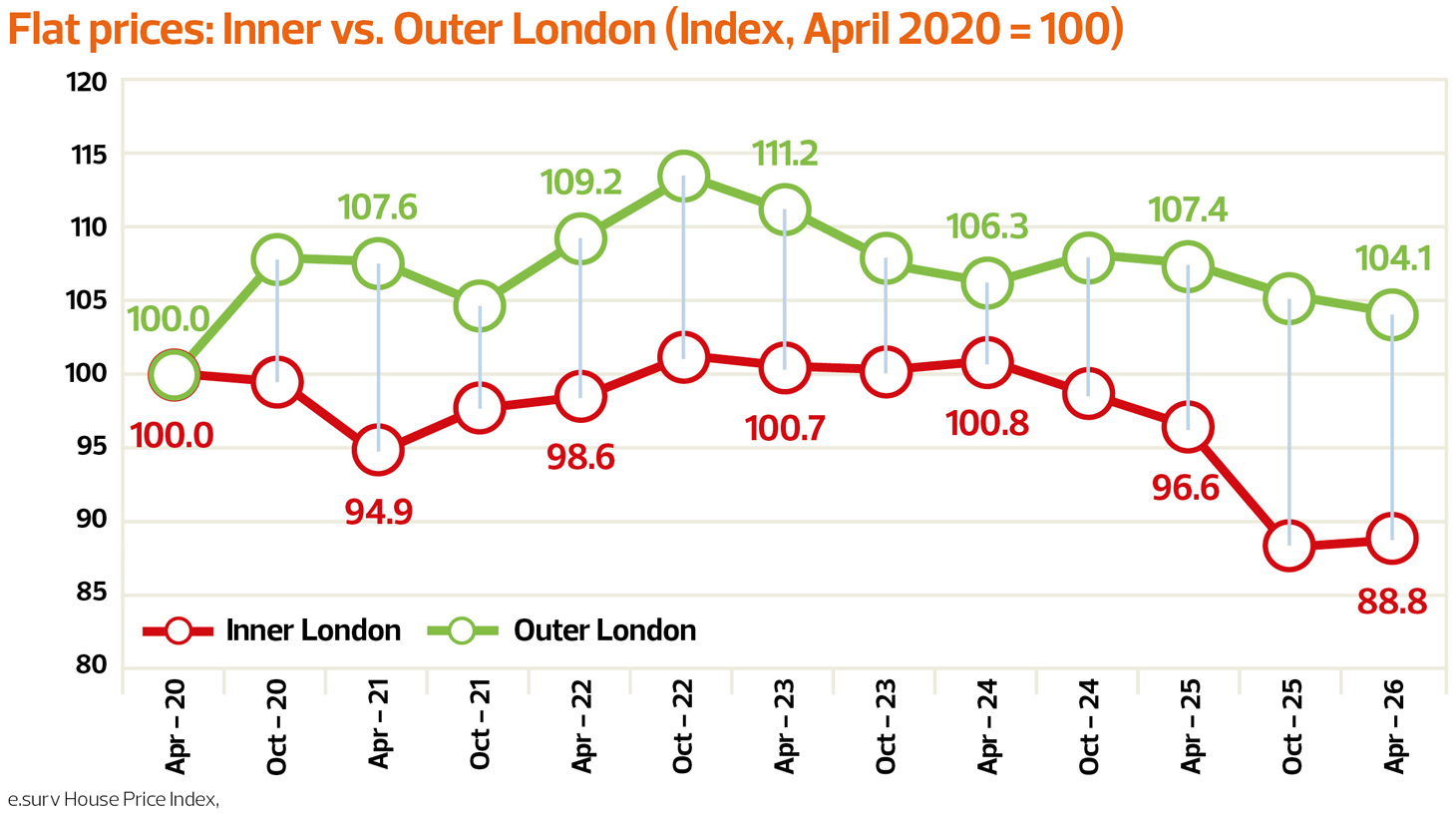

They then focus in on the flat market, which is brilliant to see as it completely changes the current rhetoric on the London Market – and the flat market.

Inner London flats under pressure

“Inner London flat prices are now 11.2% below April 2020 levels, with the index at 88.8 in April 2026. Outer London flats have softened, but remain 4.1% above their April 2020 level.

“Outer London flats rose strongly after 2020, reaching 113.4 on the index in October 2022. Prices have eased since then, but remain above the starting point. Inner London flats followed a different path, briefly returning to their April 2020 level at 100.9 in April 2024, before falling to 96.6 in April 2025 and 88.8 by April 2026.

Higher mortgage rates have had a bigger impact where prices are highest, reducing buying power for first-time buyers and mortgaged investors.”

“The weakness in inner London flats highlights several overlapping pressures. Higher mortgage rates have had a bigger impact where prices are highest, reducing buying power for first-time buyers and mortgaged investors. Higher service charges and running costs have also made some flats less attractive relative to houses or lower-density homes.

“The end of Help to Buy removed a source of demand for new-build flats, while some inner London markets continue to work through a larger supply of apartment stock.

“Tax changes add another layer of pressure at the top end. Higher stamp duty costs for overseas buyers, alongside the introduction of a ‘mansion tax’ affecting higher-value homes from 2028, are likely to be felt most in inner London, where values are highest and exposure to international buyers is greater.

“These factors are unlikely to explain the full fall in flat prices, but may be adding to caution in a market already constrained by weaker affordability and softer demand. For sellers and lenders, this points to a more price sensitive inner London flat market, where sold prices are reflecting weaker demand, higher buyer costs and increased competition from similar stock..

This is such useful insight into what’s happening at a more local level and it’s so helpful to have this insight if you are talking to buyers and sellers, or indeed the media about what’s happening!