House prices – is the foot off the gas…?

…but not on the brake, yet. Property price expert, Kate Faulkner, says the market looks like it’s about to start slowing.

Headlines

Rightmove

Price records in all regions and sectors mark ‘full house’ for first time since 2007

“The price of property coming to market has surged past last month’s record and jumped by an average of 1.8% this month. This is the highest percentage monthly rise at this time of year since October 2015.”

RICS

Buyer demand steadies while new instructions remain thin on the ground

“House price growth decelerates somewhat but remains firm right across the UK.”

Nationwide

Price of a typical UK home tops quarter of million pounds for first time

“Annual house price growth remained elevated in October at 9.9%, albeit marginally lower than the 10.0% recorded in September.”

Halifax

UK house prices hit record high as average property tops £270,000 for the first time

“UK house prices climbed again in October, as the value of the average property grew by 0.9%, an increase of more than £2,500 during the month. With prices rising for a fourth straight month, the annual rate of inflation now sits at 8.1%, its highest level since June.”

e.surv

A new normal for house price growth

“House price growth is clearly in retreat in headline terms but there is little evidence of prices stagnating or falling. Indeed, regionally, there are substantial pockets of resistance to overall falls in house price growth.”

Hometrack

No sign of ‘cliff-edge’ in buyer demand; pandemic impact on activity has further to run

“UK house price growth is currently running at 6.6% with all countries and regions of the UK registering growth rates well ahead of the 5-year annual average.”

Reports that property prices are ‘unaffordable’ continue to be wrong.

Kate says: The latest figures are a mixed bag. Rightmove is suggesting we have a ‘full house’ when it comes to price rises in all regions. Nationwide won the hearts of journalists by stating average property prices were over £250,000 for the first time, this is despite the fact that pretty much every other index, bar Hometrack, has been saying that for years. Meanwhile, some more sensible reports such as Hometrack and e.surv suggested property inflation was running more at 3-4% rather than the double digit growth everyone is mostly ‘used’ to hearing now.

Far more interesting is the impact that this has had when you look at prices over time – as a year-on-year measure is pretty poor. We can see that, despite the huge increases reported each year by many, in reality, since 2005, on average, property price rises range between 3-4%, so pretty much in line with inflation.

This suggests that many of the reports that say property prices are now ‘unaffordable’ continue to be wrong, in fact they have risen in line with inflation and, according to Nationwide, first time buyer affordability (from a mortgage perspective) remains at the long term average – around 36% of take home pay is spent on the mortgage. So, although some are using the growth over the last year as a ‘guarantee’ that there will now be a crash, price growth slowing still remains the most likely scenario for 2022.

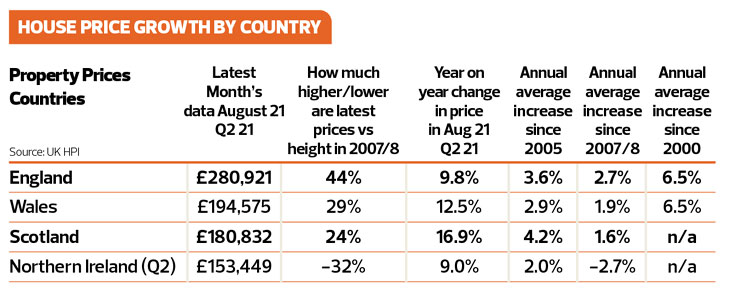

House price growth by country

Kate says: Wales and Scotland take a rare ‘starring role’ when it comes to house prices year on year – up 12.5% and 16.9% versus 2020 for Q2. What’s interesting is, this shows that the end of the Land Tax holiday in March for Scotland hasn’t really impacted on the market, in fact quite the opposite, it’s still remained pretty robust.

And, taking the e.surv Scottish report, prices were still up by 12% in August YoY. According to John Tindale, Acadata Senior Housing Analyst, “This increase in the rate of annual growth in house prices comes as something of a surprise – we had assumed that since the ending of the LBTT holiday in March 2021 prices would begin to fall gently. However, it would appear that the shift in housing preferences for larger properties – with space for home working – rather than commuting to places of work, continues to influence strongly the current housing market.”

But overall, each country is doing well, although, as ever, Northern Ireland 14 years on from the last market peak, is still seeing property prices, on average, substantially lower than 2007.

House price growth by region in England

Kate says: Although many regions are doing well – and even seeing double digit growth year on year – perhaps the ‘best performance’ is the uptick in prices in London, up by 7.5%, rather than property prices being very much in the doldrums during the pandemic, suggesting that this market may have turned.

However, forecasters are still suggesting that 2022 won’t be a great year for Londoners due to the affordability buffer they are hitting, so price rises of 1-3% on an annual basis over the next few years.

RICS

“All parts of the UK continue to exhibit strong house price inflation, with Northern Ireland, Wales and the West Midlands all seeing exceptionally firm rates according to the latest feedback.”

Halifax

“Wales remains the strongest performing nation or region with annual house price inflation of 12.9%, while Northern Ireland has recorded its strongest growth in four months (11.3%). House prices also continue to rise in Scotland, with the average property now up 8.6% year on year. In England, the North West has returned to being the strongest performing region (10.4%), which is also a four-month high. London remains by far the weakest performing area of the UK: annual inflation of just 0.8%, from an increase of 1.0% in September, is the lowest year-on-year rise in prices seen since February 2020.”

e.surv

“In general terms, all areas – except for Wales and Greater London – have seen their annual rates of growth halve over the three months, being a consequence of the ending of the stamp duty holiday for high value properties in June, since when the housing market in England has been rebalancing.

“The largest fall in the annual rate of growth was in the North East, down by 6.3%, from 9.5% to 3.2% over the month. The North East was followed by Yorkshire and the Humber, down by 5.6% from 10.6% to 5.0% over the period. In fact, 79 of the 87 unitary authorities in England, excluding London Boroughs, or 91%, saw prices fall in the month.”

Hometrack

“London is registering the lowest price inflation (2.3%) and is the only regions where growth is below the 5-year average with the demand for homes in the capital hit hardest by the pandemic.”

Property transactions – demand and supply

Kate says: Transactions are at the heart of what’s been happening to property prices over the last 18 months. Prices have been pushed up for those upsizing and downsizing thanks to great levels of equity or owning a property outright and being able to compete prices upwards for their next ‘forever home’.

When the pandemic started and there was a lot of doom and gloom, it was thought sales in the UK could halve – heading down to 600,000 instead of the average 1.2mn. In fact, we still managed to sell 1mn homes, even though we lost around two months of selling/buying during lockdown.

With this year’s transactions likely to hit 1.5 million, the industry should be congratulated for pushing through so many sales since the market opened in May 2020. It’s an incredible achievement. No, we haven’t suffered like the NHS and we aren’t ‘heroes’, but credit where it’s due, everyone has worked their socks off to get people moved during the pandemic and, done so safely.

And when you look at the average sales of 1.2mn per year, taking into account the 1mn we did in 2020, the 1.5mn we are expected to do this year, it’s not a surprise that the forecasters are feeling buoyant for 2022.

For me, I can’t believe that there won’t be some sort of slowdown, so I’m going to be bold and go for 1m transactions.

Hometrack

“The strength of market conditions are not a result of the Stamp Duty holiday alone and much bigger forces are shaping the market. This is evidenced by the fact that there has been no sign of any cliff edge in demand for homes which has been running 30% above the 5-year average since the summer. Demand looks set to end the year more strongly than last year and we expect this to carry into 2022.Q4.”

“In hindsight it is now clear that the impact of a global pandemic on the UK housing market was not going to be short lived. We believe the impact of the pandemic has further to run into 2022, supporting market activity and sales volumes. The primary catalysts will be an ongoing re-evaluation of housing needs, increased housing equity and moves in parts of the labour force to more hybrid working.

“After a record year for sales in 2021 we expect UK housing transactions to decline by 20% to 1.2m in 2022. This is in line with the long run average but still relatively high compared to sales volumes over the last decade. We do not see any important regional or country variations with sales tending to track in line with the national average.”

Rightmove

“The number of sales being agreed was up by 15.2% in September compared to the same period in 2019, which is the best ‘normal market’ comparison. This high level of demand is stalling a recovery in the depleted available stock for sale despite a continuing upward trend in properties coming to market. The latest weekly snapshot shows that the number of new sellers coming to market is still marginally down on the same period in 2019, but only by 3.2% as opposed to 9.3% for the period as a whole. This continuing imbalance, with demand outstripping supply and leading to record prices, presents an opportunity for owners looking to sell and cash out if they are downsizing or not needing to buy another property.”

NAEA Propertymark

“The average number of sales agreed per estate agent branch increased by 22 per cent from August 2021. August saw 9 sales agreed per branch and September saw that figure reach 11 per branch despite the Stamp Duty holiday end in sight.

“Sales to first-time buyers remained steady and made up 27 per cent of sales; a marginal fall from 28 per cent in August. Sales to buy to let investors fell from 11 per cent in August to 9 per cent in September.

RICS

“Nationally, the new buyer enquiries indicator posted a net balance of zero during September. This is up from -13% last month and is now indicative of a generally stable demand backdrop. The volume of newly agreed sales did slip back for a third month in succession, evidenced by -15% of respondents citing a decline (compared to -17% previously). Sales activity appears to have greater impetus at present relative to the national averages in the North East of England and Wales, where net balances of +26% and +18% were returned respectively.

“With regards to supply, the recent decline in new listings coming onto the market shows little sign of abating. The September new instructions registered a figure of -35% (compared to -36% last time) and has now been in negative territory in each of the last six months.”

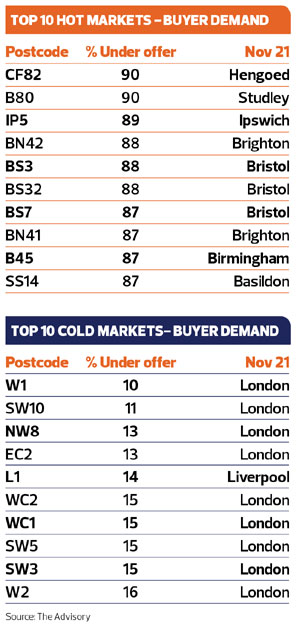

Hot and cold postcodes

The Advisory track current market conditions so buyers and sellers can gain an independent view of how easy it would be to buy and sell their home in their area. This makes it easier for good agents that are honest about market conditions to value and manage expectations.

The Advisory track current market conditions so buyers and sellers can gain an independent view of how easy it would be to buy and sell their home in their area. This makes it easier for good agents that are honest about market conditions to value and manage expectations.

From PropCast’s perspective, the hot markets at postcode level don’t necessarily track the overall increases and decreases seen even at town and city levels, with Hengoed, Studley, Ipswich and Brighton having some of the busiest markets, with London and L1 Liverpool having some of the slower ones. To find out what’s happening in your postcode visit the House Selling Weather Forecast, by Propcast.

I mentioned earlier the importance of talking to local agents to make sure you really know what’s happening locally and the ‘cold markets’ reported by TheAdvisory show why this is so important. We have seen that ‘on average’ London’ price performance isn’t great, but when you dig down into the Boroughs and postcodes, we can see that some areas really aren’t seeing much growth and may even be still experiencing falls.

The one that stands out though is L1 in Liverpool. Despite the fact that, overall, Liverpool is one of the best performing cities, there is still at least one postcode which might not be seeing growth.

Whether you are a buyer, seller or investor, the first thing you have to understand is what’s happening in your local market – are prices going up, down or staying the same. And with property prices varying so much, you need to check this out for individual property types on specific roads. Fail to do this and your sale, purchase or investment journey will be 10x harder than it should be.