PROPERTY TRANSACTION ACTIVITY: Buoyant despite higher mortgage rates

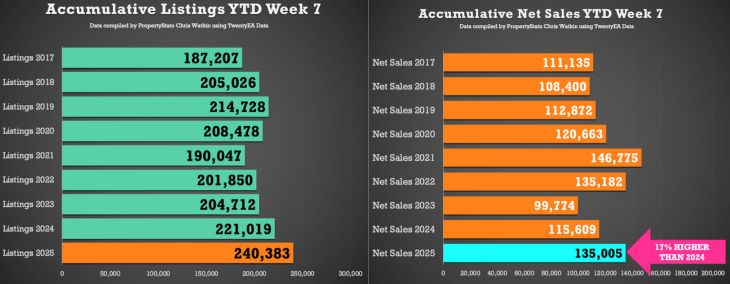

Estate agent listings are at an eight-year high, while net sales are up 17% on 2024 with offer to property transaction completion likely to rise, reports Kate Faulkner.

This year’s property transaction activity is looking pretty good and should remain buoyant for the rest of the year. Currently, agents are listing the most properties for sale for the last eight years, and the properties advertised are 9% up year on year. The good news is that although these listings aren’t all turning into as many net sales as we’ve had since 2017, net sales are still up by 17% versus 2024.

This year’s property transaction activity is looking pretty good and should remain buoyant for the rest of the year. Currently, agents are listing the most properties for sale for the last eight years, and the properties advertised are 9% up year on year. The good news is that although these listings aren’t all turning into as many net sales as we’ve had since 2017, net sales are still up by 17% versus 2024.

This is all being achieved while mortgage rates are higher than they are likely to be by the end of the year—4.5%. So, if rates do fall to their expected 4%, it should help boost demand enough to ensure that more listings are converted into sales.

Summary of the latest UK property supply and demand data

“The average number of available homes for sale per estate agency branch continues to run at a 10-year high, reducing sellers’ pricing power. Meanwhile, rising stamp duty charges are set to impact some regions and types of movers more than others. Many first-time buyers in lower-priced areas won’t be affected at all by the changes, as there is still good availability of homes that will be stamp-duty free.

“By contrast, those most affected will be first-time buyers purchasing a home between £500,001 and £625,000 where an extra £11,250 in costs is at stake for this group if the deadline is missed and not given a short extension by the government. Rightmove also expects a conveyancing log-jam as some movers scramble to complete their purchase in time.”

“HMRC monthly property transaction data shows UK home sales decreased in January 2025. UK seasonally adjusted (SA) residential transactions in January 2025 totalled 95,110 – down by -1.0% from December’s figure of 96,050 (down -17.1% on a non-SA basis). Quarterly SA transactions (November 2024 – January 2025) were approximately +0.1% higher than the preceding three months (August 2024 – October 2024). Year-on-year SA transactions were +14.4% higher than January 2024 (+20.7% higher on a non-SA basis).”

“Latest Bank of England figures show the number of mortgages approved to finance house purchases decreased in January 2025, by -0.5% to 66,189. Year-on-year the figure was +18.3% above January 2024. (Source: Bank of England, seasonally-adjusted figures).”

“The RICS Residential Market Survey results for January 2025 show buyer demand and sales easing slightly. New buyer enquiries returned a net balance of zero compared to +4% in December 2024, with agreed sales at +3%, down from +7%. New instructions returned a net balance of +25% from 14%, representing the seventh.”

“The sales market continues to register positive momentum, with all key measures of market activity running 10-11% higher than a year ago. The number of sales agreed are 10% higher, and 11% more homes are for sale than a year ago, meaning there are more buyers in the market.

While market activity continues to increase, the annual rate of house price inflation edged lower to +1.9%.”

“Increased levels of housing market activity mirrors other measures of economic activity, including robust earnings growth, higher retail sales and signs that consumer confidence is on the rise. While market activity continues to increase, the annual rate of house price inflation edged lower to +1.9% in the 12 months to January 2025, down from +2.0% in December 2024.”

“In line with seasonal trends, on average, there were around 7.8 homes placed for sale per member branch in December 2024….Market appraisal volumes provide an indicator of future supply. The average number of market appraisals conducted per member branch in December 2024 stood at 15, which is down from the previous month at 30. However, year on year represents growth within seasonal expectations.”

So far in 2025, property supply and demand are both looking good and hopefully, if demand levels remain steady, or even increase if rates fall, demand could even increase. However, we will need to see what happens with property transaction activity now the SDLT increases have returned to their long term normal rates, especially in areas like London.