SHOCK: House prices fall at fastest rate since 2011

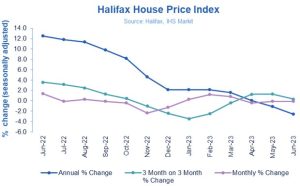

Halifax reports the largest annual house price fall in 12 years as prices slumped 2.6% in the year to June, down from a fall of 1.1% in May.

![]()

UK house prices fell last month at the fastest annual pace since June 2011 but remained relatively steady despite interest rates expected to top 6.5% by the end of the year.

Halifax reported the largest annual house price fall in 12 years as prices slumped 2.6% in the year to June, down from a fall of 1.1% in May.

Average house prices are now falling on an annual basis in most parts of the UK, with the only exceptions being the West Midlands (+1.5%, average house price of £251,139), along with marginal gains in Yorkshire & Humberside (+0.2%, £203,674) and Northern Ireland (+0.2%, £186,856).

The South of England remains the area where house prices are facing the most downward pressure. At -3.0%, the annual fall in the South East was the largest since July 2011.

London recorded an annual decline of -2.6%, its weakest performance since October 2009 and a drop of around £15,000 over the last year.

Welsh house prices were down by -1.8% annual compared to a +1.0% increase in May – the nation’s first year-on-year fall since March 2013.

And in Scotland, prices were down slightly on the year at -0.1% – the first annual contraction in property prices in the last three years.

THIRD MONTHLY FALL

Kim Kinnaird, Director, Halifax Mortgages, says: “The average UK house price fell slightly in June, down by around £300 compared to May (-0.1%) with a typical property now costing £285,932. This was the third consecutive monthly fall, albeit it a modest one.

“The annual drop of -2.6% (-£7,500) is the largest year-on-year decrease since June 2011. With very little movement in house prices over recent months, this rate of decline largely reflects the impact of historically high house prices last summer – annual growth peaked at +12.5% in June 2022 – supported by the temporary Stamp Duty cut.

“To some extent the annual growth figure also masks the fluctuations we’ve seen in the market over the past 12 months.

Average house prices are actually up by +1.5% so far this year.”

“Average house prices are actually up by +1.5% (£4,000) so far this year, with most of that growth coming in the first quarter, following the sharp fall in prices we saw at the end of last year in the aftermath of the mini-budget.”

And she adds: “These latest figures do suggest a degree of stability in the face of economic uncertainty, and the volume of mortgage applications held up well throughout June, particularly from first-time buyers.”

And she adds: “These latest figures do suggest a degree of stability in the face of economic uncertainty, and the volume of mortgage applications held up well throughout June, particularly from first-time buyers.”

Kinnaird says concerns about persistent inflation have led to a significant increase in the cost of funding and that the resulting squeeze on affordability will inevitably act as a brake on demand.

“While there’s always a lag effect when rates go up, many existing mortgage holders with variable deals or rolling off fixed rates will likely face an increase in the next year.

The squeeze on household finances will continue to put downward pressure on house prices.”

“How deep or persistent the downturn in house prices will be remains hard to predict. Consumer price inflation is likely to come down in the near term as energy and food prices look set to reverse their steep rises, but core inflation is clearly proving stickier than originally expected.

“The likelihood is that mortgage rates will remain higher for longer and the squeeze on household finances will continue to put downward pressure on house prices over the coming year.”

Serious buyers and sellers are rightly putting their confidence in the market.”

Nathan Emerson, Chief Executive of Propertymark, says: “It is inevitable that people’s finances are going to be impacted by rising interest rate, and there is a higher chance of a fall through in a sale due to the changes in buyers’ finances.

“However, serious buyers and sellers are rightly putting their confidence in the market and the majority are successfully and affordably moving home.

“Negotiations being made on properties are allowing wiggle room and bringing down the overall cost from the pandemic house price boom which was desperately needed as they were previously unrealistic and unsustainable.”

The fear factor continues to grip the UK property market.”

Chris Druce, senior research analyst at Knight Frank, says: “The fear factor over just how high the Bank of England will push the bank rate to tame inflation continues to grip the UK property market.

“While deals continue to be struck, buyers remain nervous and extremely price sensitive. This won’t change materially until we have surety about how high borrowing costs will go.

“It means that despite a period of relative stability, house prices have further to travel on their downwards journey.

“More pain will enter the system in the second half of this year as an increasing amount of fixed-term mortgages are renewed at higher rates. We expect prices will fall by 10%, spread over the remainder of this year and next.

“When stability returns, demand could prove more resilient than expected given the cushioning effect of strong wage growth, record levels of housing equity, amassed lockdown savings, the availability of longer mortgage terms and forbearance from lenders.”

We are seeing more cash buyers and house hunters who would rather buy now.”

Matt Thompson, head of sales at Chestertons, explains: “We are seeing more cash buyers but also house hunters who rather buy now before facing another potential hike in interest rates.

“This June, our branches conducted 20% more viewings than in June of last year.

“The capital’s high rents are another contributing factor to London’s continuous buyer interest.

“As tenants are facing rent increases, many are reviewing their situation and conclude that, despite higher interest rates, buying can still present a financially attractive option.”

These figures don’t yet fully reflect the recent sharp increases in mortgage payments.”

Jeremy Leaf, north London estate agent and a former RICS residential chairman, says: “This slow puncture softening in house prices reinforces the message from other recent surveys that financial markets pricing in further interest rate increases is not helping buyer confidence.

“However, these figures are a little dated so don’t yet fully reflect the recent sharp increases in mortgage payments.

“On the ground, sales are still proceeding often to those who are not dependent on mortgage finance but they are taking longer and often involve protracted renegotiations resulting in modest, rather than large, price falls.”

There is still lots of activity in the market and a fair amount of stock under offer.”

Alex Lyle, director of Richmond estate agency Antony Roberts, says: “There has been a noticeable shift in pricing compared with a year ago as the depth of demand from buyers isn’t the same and the balance of power has shifted more towards those keen to purchase. An ultra-ambitious price a year ago could well have been achieved but now that property could stick.

“That said, there is still lots of activity in the market and a fair amount of stock under offer, although chains are long and some deals are taking longer to go through than any parties would wish.

“Those buyers who have been looking for an excuse to delay their purchase and wait until we have a clearer understanding of where rates are headed, are now doing so.

“Some vendors are taking a similar approach, sitting tight and waiting until the autumn in the hope that things will have settled down by then.”

The trajectory is now almost certainly down.”

Kate Allen, founder at Devon-based luxury lettings company, Finest Stays, says: “Though house prices fell only modestly in June, the trajectory is now almost certainly down, at least during the rest of 2023.

“Much will depend on the inflation data this month, as core inflation is currently extremely sticky.

“As interest rates rise ever higher, the surge in the number of holiday homes coming onto the market in the South Hams, with most priced below the £1 million mark, is hard to miss.

“The bitter taste of remortgaging at today’s rates is proving enough to make even the wealthier people out there want to ditch the debt.

“Asking prices for good properties in prime locations remain firm but overall it’s without doubt a buyers’ market now.”This will lead to a rise in forced sales and, in some cases, repossessions.”

This will lead to a rise in forced sales and, in some cases, repossessions.”

Kundan Bhaduri, director of London-based property developer and portfolio landlord, The Kushman Group, says: “As mortgage rates increase, homeowners on ultra-low fixed rates will face challenges when transitioning to new rates this year.

“This will lead to a rise in forced sales and, in some cases, repossessions.

“The housing market’s lack of supply and new housing developments have been an ongoing issue as we know.

“This scarcity will give some resilience to house prices during these turbulent times but higher interest rates counteract those issues.

“The job market plays a vital role in supporting house prices. Stable employment and income levels provide confidence to buyers and help sustain demand in the housing market.

“Uncertainty of the nature that exists today requires landlords and home buyers to take a careful view of market dynamics and to be adaptable to these changing conditions.”

There are committed buyers who wish to move.”

And Jason Tebb, Chief Executive Officer of OnTheMarket.com, adds: “As the annual decline in average property prices continues, the high cost of living and potential for further rate rises are having an impact on how much buyers are willing and able to pay for their next home.

“However, given all the economic uncertainty it is remarkable how relatively stable the market appears to be following a period of unprecedented house price growth fuelled by shortage of new properties coming to the market.

“There are committed buyers who wish to move but they are also increasingly price sensitive. Motivated sellers must price sensibly in order to generate interest and ensure their expectations with regard to timeframes are met.”