Prices under pressure

Kate Faulkner’s monthly review of the leading house price indices shows prices are falling gently but inflation remains the problem.

The headlines

Rightmove

Demand resilient but Bank of England rate rises biting

“The price of property coming to market falls by an average of 0.2% (-£905) this month, marginally below the 0% norm for this time of year, as new sellers temper their price expectations in response to rising mortgage costs and increasing buyer affordability constraints.”

Home.co.uk

Prices flatline as stock levels surge

“Asking prices across England and Wales remain unchanged since last month, as is to be expected on the basis of seasonality, but mortgage woes will also have contributed to more conservative pricing. Meanwhile, year-on-year growth slid further into the negative (-1.5%).”

RICS

Rising interest rate expectations place renewed downward pressure on housing market activity

“The ongoing dip in national house prices appears to gain momentum slightly during June.”

Nationwide

Annual house price growth edged further into negative territory in July

“Annual house price growth edged down to -3.8% in July. This was the weakest outturn since July 2009, although it is only modestly lower than the -3.5% recorded last month.

Halifax

Slight monthly fall in property prices but housing market displays resilience

“Average house price fell by -0.3% in July, a fourth consecutive monthly decline. Property prices dropped by -2.4% on an annual basis, easing from -2.6% in June.”

E.surv

Annual house price growth at lowest rate since March 2012.

“The annual growth rate in England and Wales in July 2023, for both mortgage and cash-based house purchases, was an arithmetic average of 0.3%. This is -0.9% below the rate of 1.2% for June 2023, and represents the eleventh month in succession in which the annual rate of house price growth has slowed from the +12.8% in August 2022.”

Zoopla

House price inflation slows to +0.6%.

“Weaker demand and rising supply have driven a rapid slowdown in house price growth. UK house price inflation is currently running at +0.6% (June 2023), down from +9.6% in June 2022.”

House prices today in historical perspective

Kate says: The indices are now reflecting the slowdown in the market picked up by agents, surveyors and legal companies a few months ago. This shouldn’t be unexpected, but the movement of interest rates to 5% and now 5.25% was always going to be a breaking point in the property market as it takes mortgage rates up to and in some cases beyond the first time buyer stress tests introduced in 2014.

If priced correctly, properties are still selling.

And, bearing in mind that inflation is still running in excess of 7%, the rises in property prices of +0.5% (Rightmove) and 0.6% (Zoopla) through to reported falls of -3.8% (Nationwide) property prices in real terms are falling this year.

The good news is that although the market has slowed, according to Rightmove, if priced correctly, properties are still selling – a stark warning to agents though: Don’t take on properties that are overpriced if you are charging commission, it’ll kill your cashflow: “Properties that need a reduction in asking price are more than 10% less likely to find a buyer than those that were priced right from the start”.

Key points from leading commentators

Rightmove

- The numbers of sales agreed in June in the mid-market second-stepper sector and the top-of-the-ladder sector are 14% behind 2019’s level.

- The smaller home, two-bedrooms and fewer market sector has been less impacted, with June’s sales agreed figure 9% below 2019’s level.

- The number of available properties for sale is 12% lower than at the same time in 2019.

Nationwide

- Annual house price growth edged down to -3.8% in July. This was the weakest outturn since July 2009, although it is only modestly lower than the -3.5% recorded last month. There was a slight fall of 0.2% over the month, after taking account of seasonal effects. As a result, the price of a typical home is now 4.5% below the August 2022 peak.

- A prospective buyer, earning the average wage and looking to buy the typical first-time buyer property with a 20% deposit, would see monthly mortgage payments account for 43% of their take home pay (assuming a 6% mortgage rate). This is up from 32% a year ago and well above the long-run average of 29%.

- There were 86,000 completed housing transactions in June, 15% below the levels prevailing the same time last year and around 10% below pre-pandemic levels.

- Mortgage approvals ……showed a slight increase in activity in June, though most of these applications will pre-date the more recent rise in longer term interest rates. Activity is still c20% below 2019 levels.

Home.co.uk

- The total sales stock count for England and Wales surged above the 10-year average during June, adding around 16,000 properties to make the current total 425,624.

- The supply rate of new instructions entering the market has improved: up 11% vs. June 2022 but down 8% vs. June 2018.”

Zoopla

- +8% sales agreed in the last four weeks compared to the 5-year average but in the last two weeks, there have been some early signs of a decline in demand, dropping below 2019 levels, which is likely to increase over the summer.

- 14% fewer buyers in the market in the last four weeks than 5-year average.

- Mortgage rates moving from 4% to 5% drive an 11% reduction in buying power. The gap rises to 20% if mortgage rates move from 4% to 6%. This will not feed directly into house prices.

- The hit to buying power from borrowing costs rising from 2% to 4% has slowed the rate of price growth rather than driving sizeable year-on-year price falls.

- There are some signs that supply is starting to grow at an above-average rate with 18% more homes listed for sale in the last four weeks than the 5-year average.

Regional house prices

Kate says: It’s taken a while, but the indices are all starting to show similar figures – either insignificant rises or falls. Not surprisingly, Nationwide is reporting the most falls – ranging from -1.1% in East Midlands to a 4.7% fall in the East. The reason for this is that anyone with a mortgage will be on a tighter budget than those without, so mortgaged property prices will fall the most first.

It’s taken a while, but the indices are all starting to show similar figures.

The Rightmove index shows some rises, the most being 2.1% in Yorkshire and Humber and falls of 0.6% in London and the East. The reason this is useful data is it monitors how sellers (and their agents feel) about the up-and-coming market. Currently, their index shows some price falls, but they are still minimal and that’s likely to be due to the still tight stock levels, although we know the supply/demand balance will change over the coming months in favour of buyers.

Halifax

“Average house prices fell on an annual basis in almost all parts of the UK in July, with the only exception being the West Midlands, where they remained effectively flat. The South East remains the area where house prices are facing the most downward pressure. Down -3.9% on an annual basis, just over £15,500 has been taken off the value of a typical property in the region over the last year (average house price now £382,489). Greater London mirrors that trend, with average property prices down by -3.5% annually in the capital (average house price now £531,141).”

Zoopla

“There is a clear split between trends in southern England and the rest of the country. Higher mortgage rates have a greater impact on buying power in southern England where house prices are highest. The barriers to first-time buyers are also greater, weakening demand from buyers who support the bottom end of housing chains.

“House prices are falling by up to -0.6%, year-on-year, across all four regions in southern England as well as in Northern Ireland. In contrast, house prices continue to register annual price growth of over 1% across the other seven regions of the UK, led by Scotland where house prices are 1.9% higher than a year ago.

“We expect the divergence in house price growth between the south of England and the rest of the country to widen over the second half of 2023 with further modest price falls across higher-value markets. Some more affordable markets may not register any price falls over 2023.”

House prices in towns and cities

Kate says: Overall, out of 30 cities, since 2005, property prices have risen above inflation in nine cities/towns, including Leicester and Milton Keynes, on par with inflation is Croydon and Tunbridge Wells, and in all the remaining towns and cities, price growth has remained below inflation. Even with the price growth seen during the pandemic, what this shows is that, in real terms, especially for those that own outright the property they have isn’t necessarily delivering from an investment perspective.

E.surv

“In June 2023, 65 of the 110 Unitary Authority areas in England and Wales were still recording house price gains over the previous twelve months, indicating the wide extent to which price rises have been taking place across the two countries, even if the growth rate is now diminishing.

“The area with the highest annual increase in prices in June 2023 is Hartlepool, at 16.4% growth – the average price being assisted this month by the sale of a detached home located in Wynard for £910,000.

Zoopla

“Drilling below the regional level, it’s clear that housing markets with average prices over £300,000 are feeling the impact of higher mortgage rates more than other areas. Some 4 in 5 local markets currently registering annual price falls have average prices over £300,000. The chart below shows annual price growth compared to average house prices for 121 UK postal areas in June 2023.

“Higher house prices mean larger mortgages, bigger deposits and a higher household income required to buy a home. The more the income needed to buy increases, the more households are priced out of the market, which reduces demand and pushes prices lower.

“Markets across South East England are leading on annual price falls, particularly in commuter markets adjacent to London. These are led by SS – Southend (-1.5%), WD – Watford (-1.2%) and HP – North West Hertfordshire (-1.1%).

Demand and supply

Kate says: Despite much of the media focusing on property prices, from a buyer’s/seller’s perspective, for the industry and indeed for the economy, what’s more important is the data we receive on transactions.

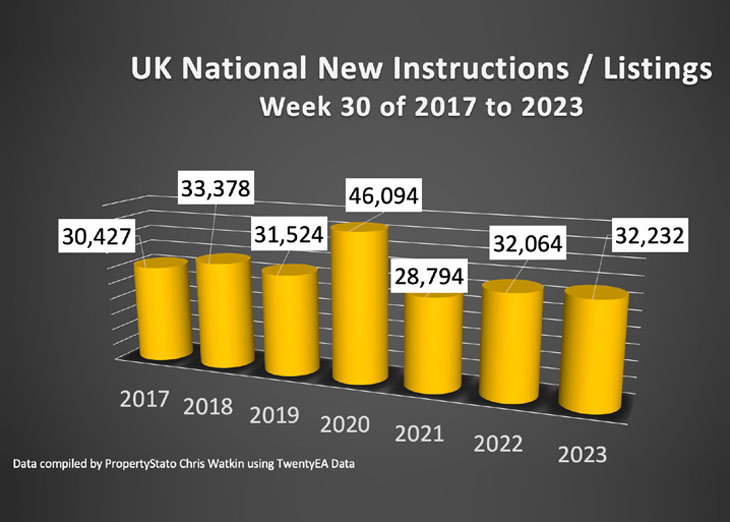

As the fabulous tables from Christopher Watkin and TwentyEA show, the number of new instructions is pretty consistent over the years, bar the wobbles we had during the pandemic. In fact, the new instructions are pretty bang on the average from 2017 to 2019.

From a sales agreed perspective, it’s not a surprise this has taken a bit of downturn versus the pre-pandemic years now bank base rates have reached 5% and beyond.

I did think that the Bank of England would do the sensible thing and hold rates in July, but as they have risen again, it’s almost immaterial how much they go up to now – for buyers, because moving rates to 5% which pushes mortgage rates from 6-7% means a lot of the stress testing for FTBs introduced in 2014 is being surpassed, reducing the number of buyers in the market.

All any rate rises will do now is make things a lot worse for the 7% of households (2mn out of 28mn) that are coming off their fixed rates over the next year (including renters), the other 93% aren’t likely to be as affected at all, and as a result, it’s likely to have much less impact on reducing inflation further.

Sales-wise, up until the 5% bank base rate, we were doing pretty well under the circumstances – around a 6% fall, but as Zoopla have indicated “… in the last two weeks, there have been some early signs of a decline in demand, dropping below 2019 levels, which is likely to increase over the summer.”

And although these stats show that hasn’t changed much, looking at latest sold date since the June bank base rate rise, sales are definitely falling.

Commentaries on demand and supply

TwentyCI

“At the time of publishing, there were 635,901 newly instructed properties on the market. This is 27,947 more than reported in our June Pulse. There were also 19,794 more properties sold subject to contract in June (426,008 compared to 406,214). However, there were 3,929 fewer properties exchanged (182,684 compared to 186,613 in June).

Propertymark

“The supply of new homes up for sale per member branch continued to lessen in June – now at eight per member branch. A summer lull is generally expected. On the other hand, the average number of sales agreed per member branch held at seven in June—the same figure as the previous month. Total stock of properties available per member branch fell slightly to 32 on average in June compared to 36 in May. Properties available for sale remain 23 per cent higher than in June 2022.”

Zoopla

“Demand for homes recovered over 2023 H1 as mortgage rates fell towards 4%, supporting an increase in new sales. Mortgage rates rising quickly over the last six weeks towards 6% has reduced buying power and hit demand, which has fallen by 18% over the last 2 months.

“The decline in demand is less stark than that recorded in the wake of the 2022 mini-budget or when the first lockdown was introduced. Demand has weakened off a lower base and is currently running 6% below 2019 levels. Year-on-year, demand is down 40% but sales agreed are only 17% lower, yet we see more committed sellers and buyers in the market.”

Where is the market going?

Kate says: The likelihood is that we will now slide, so it’s definitely a ‘game of two halves’ this year. The first six months, surprisingly robust, the second will be a bit tricky. I expect a quiet summer, the market will pick up a bit from mid September for those keen to move before Christmas and then very little work in November and December for most areas and property types – although this will be very individual.

Critical to the success of the market from now on is agents and sellers pricing properties realistically, otherwise agents are just going to list impossible to sell properties and are likely to run out of cash pretty soon.

Nationwide

“Investors’ views about the likely path of UK interest rates have been volatile in recent months, with the projected Bank Rate peak fluctuating between 5% in mid-May and 6.5% in early July (see chart below).

There has been a slight tempering of expectations in recent weeks but longer-term interest rates, which underpin mortgage pricing, remain elevated.

Zoopla

“The outlook [for H2] for market activity and prices depends on the trajectory of mortgage rates. It will be influenced by market expectations for how much higher base rates are likely to increase to control inflation.

The latest inflation reports are starting to show the impact of higher base rates feeding through into the economy. It looks less likely that the Bank of England will need to raise rates as much as financial markets expected just a few weeks ago.