Holding up

It’s a complex picture and there are more downs than ups, says housing market expert, Kate Faulkner, but overall the market is taking the strain.

The headlines

Rightmove

1.9% summer price drop as stretched affordability begins to improve. Average new seller asking prices fall by 1.9% (-£7,012) this month to £364,895, the biggest fall in August since 2018, as summer sellers tempt buyers preoccupied by holidays, inflation, and the highest Base Rate since 2008.”

Home.co.uk

Prices hold firm in the North but slide in the South. “Asking prices across England and Wales have taken what could be regarded simply as a seasonal dip of 0.3% since last month, although at the same time rising mortgage costs are inevitably dampening vendors’ expectations, most notably in the South.”

RICS

Tighter lending environment continues to weigh heavily on home buyer activity. “National house price indicator retreats further over the month.”

Nationwide

August sees further weakness in house prices. “August saw a further softening in the annual rate of house price growth to -5.3%, from -3.8% in July, the weakest rate since July 2009. Prices fell by 0.8% over the month, after taking account of seasonal effects.”

Halifax

UK house prices fell in August as impact of higher rates flows through. “On an annual basis prices fell by -4.6%, the biggest year-on-year decrease since 2009, though it should be noted that this is relative to the record-high property prices seen last summer.”

Zoopla

Annual UK house price inflation slows to +0.1%, lowest since 2012.“While house price growth has slowed rapidly over the last year, the primary impact of higher mortgage rates has been lower sales volumes.”

Kate says: Reading the reports and headlines this month, it’s really important to remember where the data is coming from and making sure the headlines match. For example, the Nationwide and Halifax falls are being reported as ‘house prices are falling by….’ But that isn’t accurate, they are reporting mortgaged property prices ONLY.

Average house prices are still 19% higher than pre-pandemic.

Bearing in mind that 30%+ sales are cash, in my view it is incorrect to say ‘house prices’ are up or down by xx%, mortgaged property prices maybe, but cash sales can and are reacting very differently!

Key points from the leading indices

Rightmove

Despite the ‘doom and gloom’, Rightmove reminds everyone that average prices are still £59,000 (19%) higher than in the pre-pandemic market of August 2019.

“The average five-year fixed mortgage rate is now 5.81%, falling from 6.08% this time just three weeks ago and currently showing signs of an improving trend.

“A key factor preventing more significant price falls so far this year is that the number of available properties for sale remains historically constrained and is currently 10% lower than in 2019.”

Nationwide

“In the first half of 2023, the number of completed housing transactions was nearly 20% below pre-pandemic (2019) levels and c.40% lower than in the first half of 2021 – though the latter reflects the boost to activity from pandemic-related shifts in housing preferences, the Stamp Duty holiday and ultra-low borrowing costs.

“Home mover completions (with a mortgage) in the first half of 2023 were 33% lower than 2019 levels, whilst first-time buyer numbers were c.25% lower. Buy-to-let purchases involving a mortgage were nearly 30% below pre-pandemic levels. By contrast, cash purchases were actually up 2%.”

Halifax

“Income growth has remained strong over recent months, which has seen the house price to income ratio for first-time buyers fall from a peak of 5.8 in June last year to now 5.1. This is the most affordable level since June 2020, and will be partially offsetting the impact of higher mortgage costs.”

Home.co.uk

“Key indicators such as marketing times and stock levels continue to weigh in lower than observed in pre-COVID years 2018 and 2019. Meanwhile, following the December 2022 drop, pricing remains relatively firm overall with no notable increase in price-cutting of on-market properties.

“The Typical Time on Market for unsold property in England and Wales increased by just two days during July, consistent with seasonal expectations. The current median is a relatively healthy 80 days, which is considerably lower than at any point during pre-pandemic 2019.

“The supply rate of new instructions entering the market remains very restrained: down 2% vs. July 2022 and don 4% vs. July 2018. The largest year-on-year rise was in the East of England (+5%).”

“Looking at the real home price growth chart, we can clearly see that significant falls in real terms began around April 2022 and a major price correction has been taking place ever since, with the greatest monthly falls around March this year.”

Zoopla

“Market activity continues to track in line with 2019 levels but remains well below levels of activity recorded over the more recent pandemic years.

“All regions across southern England are registering year-on-year price reductions of up to -1%. All other regions and countries of the UK are posting low, single digit price growth. Scotland is registering growth of +1.7%.

“Our view that price reductions will remain concentrated across southern England where affordability challenges are greatest. Lower house prices and mortgage rates are needed to stimulate demand and sales.

“Our data on the number of homes being sold ‘subject to contract’ over the year to date shows the market is still on track for 1m sales completions in 2023.”

Regional property prices

Kate says: The property market is typically very difficult to report on ‘in summary’, especially when it’s ‘going up’ and ‘going down’ as what’s happening is so individual to a property not just to an area. Prices then depend on whether you are buying with cash or a mortgage, so even regional reporting isn’t likely to be that helpful to buyers, sellers and investors.

Add to this, as all the indices measure the market at different times and in different ways (some UK, some England and Wales, some mortgaged only) their reports of prices being up and down are all over the place just now and it will take a few more months until we see some consistent reporting across the indices. Hence, the North East is being reported as up by 4.7% according to the Land Registry, up by 2.6% (Rightmove), up by 1.8% according to Home but down by 3.3% according to the Nationwide. A range of price reporting from -3.3% to 4.7% is huge!

However, the main ‘summary’ that you can conclude from the regional data is that areas which are typically high priced and require a mortgage are suffering a lot more, hence the ‘north-south divide’ is coming back into play.

It’s important to constantly remind local media, buyers and sellers that whatever is being ‘reported’, within each region, prices are likely to be going up, down and staying the same, or at least the last the two just now!

Zoopla

Southern regions register the larger price falls

“There is a clear north-south divide in house price inflation. All regions across southern England are registering year-on-year price reductions of up to -1%. All other regions and countries of the UK are posting low, single digit price growth.

“This pattern of price changes reflects the greater impact of higher mortgage rates on higher-value housing markets. Buyers in southern England need larger mortgages, bigger deposits and higher incomes to buy. This prices more buyers out of the market, weakening demand and pushing down prices.”

Prices holding up where FTBs can still buy

“We believe that the variation in house price growth across the UK is partly explained by the ability of first-time buyers (FTBs) to buy at higher mortgage rates. FTBs account for 1 in 3 sales a year, most of whom originate from the private rental market. This means the dynamics of renting and buying will impact on demand and prices.

“Low mortgage rates over recent years made mortgage repayments for buying much cheaper than renting. This supported FTB demand and led to many FTBs opting to buy 3+ bed homes, bypassing the market for flats and smaller houses. Mortgage rates over 5% have now reversed this trend at the national level, making renting 10% cheaper than buying at a UK level, despite high growth in rents in recent years.

“However, the experience for would-be FTB buyers varies across the UK. A renter buying the home they rent would find it cheaper to buy than rent in the six regions and countries with the lowest house prices. In Scotland and the North East average mortgage repayments are up to 18% lower than rental costs. This supports access to the housing market and the demand for homes.

“In contrast, it is more expensive to buy a home than to rent across all areas of southern England and Midlands. In London, the average monthly payment is 24% higher than the monthly rent. Higher mortgage rates are pricing more FTBs out of the sales market across southern England, reducing demand and compounding the downward pressure on house prices.

“The actual position is worse for all FTBs when allowing for the fact that mortgage lenders require new borrowers to be able to afford higher ‘mortgage stress rates’ of closer to 8.5% rather than the product rate of 5.6% used in this analysis.

Towns and cities house prices

Kate says: Overall, out of 30 cities, since 2005, property prices have risen above the average 3.8% inflation in ten cities/towns, including Manchester and Milton Keynes, on par with inflation is Tunbridge Wells. All the remaining towns and cities, price growth has remained below inflation. Even with the price growth seen during the pandemic, what this shows is that, in real terms, especially for those that own outright the property, they have isn’t necessarily delivering from an investment perspective.

Demand and supply

HMRC

“July is the second consecutive month in which we have seen a small increase in seasonally adjusted transaction figures. Seasonally adjusted residential transactions are up 1% relative to June.”

Figure 1: Non-seasonally adjusted and seasonally adjusted UK residential property transactions by month between July 2020 and July 2023.

Propertymark

“The supply of new homes placed for sale per member branch showed a positive lift in July – now at ten per member branch. The average number of sales agreed per member branch also showed an uplift to eight in July. The total stock of properties available per member branch climbed slightly to an average of 38 in July compared to 32 in June. Properties available for sale show a 37 per cent jump year on year and prove to be at their highest level across the last twelve months. This is proving that resilience and determination to move home remains within the market.”

ales fallen since rates hit 5%

(Data from Christopher Watkin and TwentyEA.)

“As you can see from the chart below, new instructions are actually holding up pretty well this year. What we aren’t seeing is a huge rise in listings due to a fear of mortgage rises nor are we seeing huge amounts of sellers holding off putting their property on the market now it has slowed. So currently, on a listing basis, things are ‘pretty normal’.

“From a sales agreed perspective (the pink line), not surprisingly this shows that we aren’t selling as many properties as we have by this time in previous years and are certainly heavily down year on year. Cumulatively we are still only down by 6% versus ‘more normal’ years from 2017 to 2019, which considering the cost of living crisis and the mortgage rate rises is amazing.

“However, we saw an immediate drop in sales the week after bank base rates hit 5% and with the current 5.25% rate and this is definitely causing a much tougher market slow down than we’ve seen so far this year.

“This is reflected sales wise in week commencing 21st August. Versus 2017 to 2019 sales are down from an average of 23,266 for the week to 20,304, which is double the previous dip we’ve seen: 12.7% fall vs 6% to date.”

TwentyEA

“At the time of publishing, there were 634,854 newly instructed properties on the market. This is 1,047 fewer than reported in our July Pulse.

“There were 1,019 more properties Sold Subject to Contract than in July (427,027 compared to 426,008). There were also 9,671 more properties exchanged in May, June and July (192,355) compared to April, May and June (182,684).

“In July, the South East led the way once again, reporting 103,747 available for sale. This was followed by the East of England with 70,597 for sale. The North West surpassed Inner London in July, registering 67,158 for sale, compared to Inner London’s 66,856.”

Nationwide

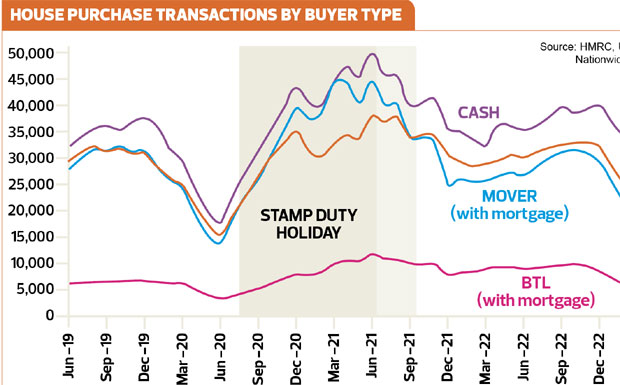

Cash transactions proving more resilient in a sluggish market

“In the first half of 2023, the number of completed housing transactions was nearly 20% below pre-pandemic (2019) levels and c.40% lower than in the first half of 2021 – though the latter reflects the boost to activity from pandemic-related shifts in housing preferences, the Stamp Duty holiday and ultra-low borrowing costs.

“An examination of the composition of transactions reveals that cash purchases, though down from the 2021 highs, have been remarkably resilient, while purchases involving a mortgage have slowed much more sharply.

Where is the market going?

Kate says: I predicted a slowdown in the market over the summer and that’s definitely happened. I think that we’ll see a little more activity September/October, especially with the more competitive mortgage rates released over the last few weeks. If we have ‘peaked’ rate wise, that will definitely help the market recover, but I do expect November and December to be pretty quiet as more homeowners end up paying higher mortgage rates, people will face still high energy and food costs and are likely to focus on getting through Xmas rather than moving home.

RICS

“Looking ahead, national price expectations remain negative at both the three and twelvemonth time horizons. For the year ahead, a balance of -49% of contributors anticipate a further fall in house prices. While the latest reading is identical to last month’s figure, it denotes a considerable dip relative to the flat reading of -3% returned in May prior to the most recent shift in interest rates.”

Nationwide

“While activity is likely to remain subdued in the near term, healthy rates of nominal income growth, together with modestly lower house prices, should help to improve housing affordability over time, especially if mortgage rates moderate once Bank Rate peaks.”

Zoopla

While first-time buyer numbers will be lower in 2023, we expect them to hold up as a result of more flexible working opening up options to buy in cheaper markets as well as buying costs being lower than renting in more affordable markets. In addition, more landlord selling previously rented homes, which are typically priced 25% lower than the wider market, is boosting available supply that appeals to FTBs.

“Mortgage rates are starting to drift lower but remain over 5%. We expect them to fall below 5% later this year but it looks set to be a drawn-out process as the financial markets re-evaluate how much longer interest rates need to remain higher to bring inflation under control. Any further improvement in affordability from lower mortgage rates is unlikely to impact on the market until 2024 H1.

“While house price growth has slowed rapidly over the last year, the primary impact of higher mortgage rates has been lower sales volumes. Our data on the number of homes being sold ‘subject to contract’ over the year to date shows the market is still on track for 1m sales completions in 2023. This will be 21% down on 2022 levels and the lowest number of sales since 2012. It’s the equivalent of the average household moving once every 23 years.”