PROPERTY MARKET LATEST: Is this 2008 all over again?

Property market expert, Kate Faulkner, reveals that the latest indices suggest we are experiencing similar activity to what happened before prices slid backwards in 2008.

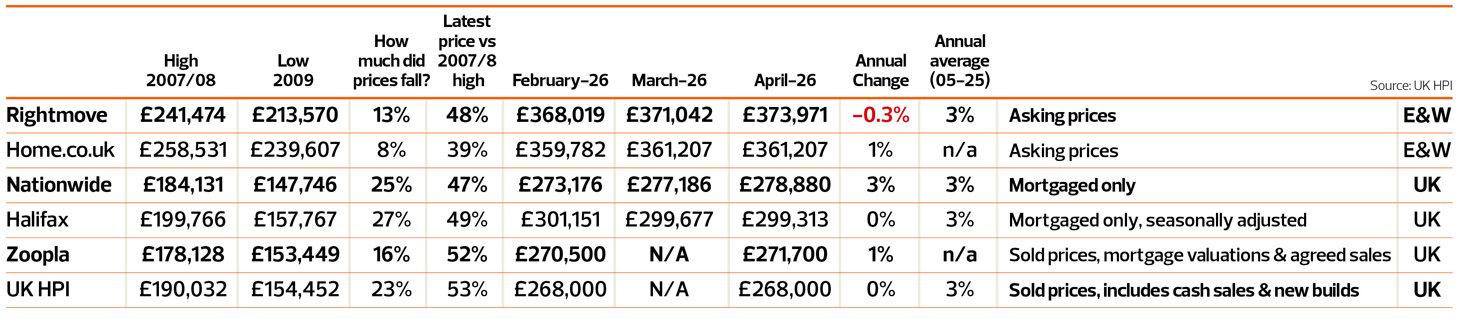

Although the national average figures for pretty much every property market measure show the market is being ‘resilient’ at the moment, despite huge Global and National economic headwinds, it really does depend on where you operate at the moment.

Although the national average figures for pretty much every property market measure show the market is being ‘resilient’ at the moment, despite huge Global and National economic headwinds, it really does depend on where you operate at the moment.

We have stats this month that show areas to the North and West continue to perform well, while London, East Anglia and the South are still struggling to see prices get back to where they were back in 2022.

What’s more interesting though is that regional geography doesn’t tell the full story at all. E.surv have produced some great data this month comparing Inner and Outer London and that suggests average London figures are being dragged down by the Prime Market – as well as insightful information on flat prices too.

However, key to whether we have good or poor market performance as we move into the second half of this year is very much down to what happens next in the US/Iran War – and the answer to that is ‘goodness knows’ and I think it’s highly likely Mr Trump does either!

Thankfully, the property market indices and their experts have knocked it out the park in their commentary on this, this month, so here’s a summary of their excellent insight, which includes some suggesting that we are at a similar time to what happened before prices slid backwards in 2008!

Insights from the property market indices

Sales stock surge while London prices slide

“The current situation reminds me of the surreal beginning of the 2008 crisis. Prices remained suspended in thin air for quite some time before the true reality of the situation sent prices tumbling. Current pricing seems to be based expectations of a re-opening of the Strait relatively soon and a return to previous energy prices. Unfortunately, this scenario is looking less and less likely. The longer the Strait of Hormuz remains effectively closed the worse the fallout will be.

“The money markets have already priced in two hikes in the UK Base Rate before the end of the year and there may well be more to come as the Bank of England clumsily attempts to deal with inflation. Moreover, we may have more nasty surprises to come. Rising bond yields are signalling a possible sovereign debt crisis for heavily indebted countries. We had a brief taste of this with the Truss ‘mini-budget’ debacle, but this time around no UK Treasury policy changes will be effective in dealing with the cause of the problem in the Persian Gulf.

“Even if the Straits were to open now the damage to both production and global supply is already done and it would take a year or so for energy and fertiliser markets to return to a more normal state of affairs. The upshot for the UK property market is a looming market correction where serious vendors will cut their asking prices to sell and others will abandon their sale, perhaps turning to the rental market despite its current poor performance.”

Robert Gardner, Nationwide’s Chief Economist

House price growth remained resilient in April

“The market is likely being supported by the relative strength of household finances. In aggregate, household debt is at its lowest level relative to income for around two decades, and sizeable savings buffers have been built up in recent years, although these have not been evenly distributed across households.

“Looking ahead, UK economic growth is likely to be somewhat weaker and inflation higher than previously expected as a result of developments in the Middle East, although the ultimate impact will depend critically on the duration of the shock and the policy response.

“However, the UK economy and housing market have proved remarkably resilient in recent years. This provides some confidence that, if the latest shock passes relatively quickly, and energy prices normalise in the quarters ahead, any near-term softening in the housing market will also prove short lived.

Amanda Bryden from the Halifax

House prices remained broadly stable in April

“A slower pace of house price growth may be disappointing news for existing homeowners.” She explains: “However, for those looking to step onto the property ladder, stable prices are helpful, even if higher mortgage rates mean affordability remains stretched. The average price paid by first time buyers has fallen slightly to £238,908, its lowest level so far this year.”

“The upside scenario is that more sellers entering the market supports transaction volumes even in a lower-demand environment, and committed movers continue to transact. The market can sustain current activity levels if stock is priced correctly and buyer finance is in place.”

“The number of homes for sale is at its highest level for this time of year since 2015, and almost a third of listings of existing homes for sale are seeing prices reduced. In light of this, new sellers need to price carefully at the beginning of the process to avoid longer selling times. Homes that didn’t need a price reduction sold in just 36 days, compared with 127 days for those that needed a reduction. “

GB market: prices still rising, but slowly

“The picture is not one of broad-based weakness, but increasing divergence. Growth remains modest overall, but pressures are concentrated in London – particularly in inner boroughs and the flats market – while more affordable areas continue to hold up. Affordability, rather than demand, remains the key constraint.”

Be optimistic

My thoughts? I am an optimist and I do think the Iran/US war has to be solved soon or the mid-terms are going to be disastrous in America for Trump. It won’t change things immediately, but it will improve confidence and mean we can all go back to planning for the future rather than being stuck in the uncertainty around the cost of living – and doing business.

It’s also important to remember that today’s market is very different from that of 2008.”

It’s also important to remember that today’s market is very different from that of 2008. Mortgage lending is far more tightly regulated, and borrowing levels are nowhere near the excesses seen before the financial crisis. First time buyers, for example, have generally been taking out repayment mortgages since 2014, helping them build equity rather than relying on interest-only borrowing.

In addition, more than half of homeowners now own their property outright, reducing the number of people who may be forced to sell during periods of economic uncertainty. Many borrowers are also protected by fixed-rate mortgages, while lenders and government-backed support schemes have increasingly focused on helping households remain in their homes. In most cases, it is more cost-effective for everyone involved to support borrowers through financial difficulties than to pursue repossession.

That said, property markets are always local. What happens in one town, city or even postcode can be very different from the national picture. That’s why it’s essential to lead conversations about what’s happening in your own market, rather than relying solely on the regional or national headlines reported in the media.