Under pressure

Kate Faulkner of Propertychecklists.co.uk analyses the leading house price indices – pressure is easing, but not by much.

Headlines

Rightmove

Fifth price record this year but further signs of pace easing

“Price of property coming to market hits a fifth consecutive record of £368,614, albeit only up by a modest 0.3% in the month, as the pace of price growth slows.”

Home.co.uk

Inflation outpaces home price growth

“Asking prices across England and Wales surged a further 0.9% overall in May, bringing the year-on-year rise to 6.5% while inflation leapt to 13% (RPI ex. housing).”

Nationwide

Annual house price growth slows in June, but remains in double digits

“Modest slowing in annual UK house price growth to 10.7% in June, from 11.2% in May.”

Halifax

House prices continue to increase as market shows resilience

“The UK housing market defied any expectations of a slowdown, with average property prices up 1.8% in June, the biggest monthly rise since early 2007. This means house prices have now risen every month over the last year, and are up by 6.8%.”

E.surv

Annual price growth increases to 9.8% in England and Wales

“The average price paid for a home in England and Wales in May 2022 was £373,471, up 1.0% on the average price paid in April. But if we look back to March 2020, we can see that prices are now some £57,600, or 18.2%, above those at the start of the pandemic.”

Zoopla

Average house price hits all-time high, but market starting to soften

“Average house prices were broadly unchanged in May, rising by just 0.1%. This is the lowest rate of monthly price growth since December 2019. Growth on a quarterly basis, at 1.4%, is the slowest rate of in 15 months. In total, average prices are up +8.4% on the year, taking the average UK house price to £251,550.”

The national picture in historical perspective

Kate says: For years since the credit crunch, property price growth was rising at levels typically below inflation, having beaten it for many years. However, the impact of the pandemic with huge rises in most areas (but not everywhere!) shows this is having a positive impact and taking property back into inflation beating growth for the first time since 2007.

Kate says: For years since the credit crunch, property price growth was rising at levels typically below inflation, having beaten it for many years. However, the impact of the pandemic with huge rises in most areas (but not everywhere!) shows this is having a positive impact and taking property back into inflation beating growth for the first time since 2007.

Annual rate rises by all the indices are now moving from less than 3% growth to 3.5% or just over 4%. However, with inflation rising this year, it may be that by the end of the year, with price growth forecast to fall back (but not fall) this might just tip property back into an asset that has ‘on average’ underperformed versus inflation.

And most of the reports are now agreeing – property price growth is reducing. According to Rightmove “despite five consecutive interest rate rises and the increasing cost of living, buyer demand for each available property remains very strong, being more than double (+113%) the pre-pandemic five-year May average. However, we are seeing signs that this is continuing to ease, with this measure down by 8% in May compared to April.”

Start now if you want to move before Christmas!

Gráinne Gilmore Head of Research for Zoopla concludes, “Sales market conditions are strong by any measure, but there are signals that the impetus in the market is slowing, and more price sensitivity in the market will spell a slowdown in price growth during the remainder of 2022”

Other evidence for a slowdown from Zoopla is the time it takes to sell a property is rising: up to 22 days in May from 20 days in March. And the length of time it is taking to sell a property is leading both Rightmove and Zoopla to suggest that anyone wanting to sell before Xmas needs to get their skates on. Rightmove suggests that the “conveyancing log-jam means sellers need to come to market in the next few weeks to be in with the best chance of moving before Christmas, with the average time to get through conveyancing currently 150 days”.

While Zoopla explain “The average time taken from searching for a home to exchange, at which point buyers can move in, is now averaging around 170 days – around five and a half months”, signalling that those who want to move this year need to consider commencing their search, and their home sale now, or it could be 2023 before they get to move.

But none of this should be seen as ‘bad news’ from an agent and industry perspective with “more than 500,000 homes currently sold subject to contract” so far this year, signalling growth of 44%+ than 2019 (Rightmove).

Overall, despite the slowdown and the cost of living crisis, Nationwide’s view is that, “Part of the resilience is likely to reflect the current strength of the labour market, where the number of job vacancies has exceeded the number of unemployed people in recent months. Furthermore, the unemployment rate remains close to 50-year lows. At the same time, the stock of homes on the market has remained low, which has helped to keep upward pressure on house prices…

“The market is expected to slow further as pressure on household finances intensifies in the coming quarters, with inflation expected to reach double digits towards the end of the year. Moreover, the Bank of England is widely expected to raise interest rates further, which will also exert a cooling impact on the market if this feeds through to mortgage rates”.

So, despite some doom mongers in the market predicting a crash, it looks like 2022 activity will remain strong – not even rocked by the latest government chaos which has decimated those ‘in charge’ of the housing market!

Property prices, nationally

Kate says: Both Wales and Scotland top the property price growth year on year according to the Land Registry with rises of 16%+. Although this is a lot higher than the Nationwide’s measures which suggest Scotland is one of the worst performers – growing at just 9.4% versus the inflation busting 13.4% for Wales – although still not a bad performance!

Over time though, despite UK growth now beating average inflation of 3% each year, Wales has only just kept up with inflation while England and Scotland have leapt ahead and Northern Ireland continues to lag behind due to the huge falls seen during the credit crunch.

Property prices by region

The various indices are tracking different rates of growth across the regions. The highest growth is reported in the South West by most reports. And this shouldn’t be a surprise as according to Zoopla, “The fastest-moving market is in the South West, with the average length of time taken between listing and agreeing a sale less than three weeks (19 days). This reflects the high levels of demand in the South West since the start of the pandemic, as some buyers making a move prioritise access to rural and coastal settings“.

In other regions, Zoopla reports that, “Homes in London are staying on the market longest, with 35 days between listing and sale agreed – although this is still a large reduction on the 5-year average of 50 days to agree a sale”. And this is reflected in price growth with London being the worst performer of all regions, reporting anything from 3.3% growth by Home.co.uk through to Nationwide’s 6% growth for mortgaged properties, and the Land Registry’s 7.9% rise which includes cash buyers.

Wales and Scotland top the property price growth year on year – Land Registry.

It is interesting to see that both mortgage related property purchasing indices: Nationwide and Halifax are pretty similar in their growth rates by region year no year. While the Land Registry and Rightmove report wider growth differentials and Home.co.uk (and indeed Zoopla for cities) are reporting much lower growth, likely because they are taking into account the higher proportion of house sales versus flats.

And of course, the house price averages are hugely different. London sees the biggest differential, ranging from £530,000 for the Land Registry through to £682,000 for Rightmove. This shows that using regional averages to reflect what’s happening in markets for consumers is a poor way to inform buyers and sellers of what’s actually happening for them and can put them off buying or selling.

Towns and cities, price tracking

Kate says: As with the regional data, we continue to see huge variations across the towns and cities we track in the table below.

The worse performer over time is Belfast which was devastated by the credit crunch. Property prices dropped by 59% – nominally, so this doesn’t include inflation – and are now still 28.6% lower than the average price in 2007/8. Although there may be some excitement in the area that they are seeing 6.8% rises year on year, over time, property prices since 2005 have only increased at 2.2% annually, so prices here have performed at levels way below inflation, bad news for those who own their property outright.

On this basis the best performers may be a bit of a surprise. Manchester is actually the winner – 5.2% growth since 2005, followed by Cambridge at 5.1% and coming in third is London’s at 5% annual growth over time. Bristol’s grown at 4.8% per annum and Brighton and Hove, Milton Keynes, Edinburgh and Oxford have all grown in excess of 4% year on year, beating inflation of around 3%.

However, there are still places that look good year-on-year, but have not performed well historically. These include Nottingham which is topping the price charges for Zoopla this month, but over time has only increased by 2.9% – almost half the rate of other cities.

Property averages are useful for comparisons and discussion, but they are never any real use to buyers and sellers.

Demand and supply

As most of the reports are suggesting, we are seeing a slight improvement to demand versus supply. However, it’s nothing to get too excited about as the imbalance – both in the sales and rental markets is getting to serious levels now.

Blaming agents, developers and buy to let investors for the problems has to now stop and the real issue causing the housing supply problem: no one in government or at local authority level has taken proper responsibility for delivering the housing the nation needs.

Increasing the supply of affordable homes for both sale and rent is the responsibility of government and local authorities and they have clearly failed, not least because of the revolving door of housing ministers and secretaries of state.

Love or hate Mr Gove, he did seem to be ‘a doer’ and it’s a shame he got caught up in this latest government chaos. Let’s just hope when we get a new Prime Minister we can get back to the government’s job: putting affordable roofs over people’s heads and this chopping and changing stops for a short while at least.

Stock levels

Propertymark NAEA is reporting, “There were nine sales agreed on average per member branch in May—the same number as in April. This figure is also in line with the pre-pandemic average for May of nine (based on 2010–2019 figures). With such high demand, we may expect sales to be higher. But the lack of supply is keeping the total sales in check).”

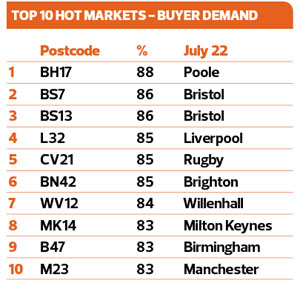

Postcodes – hot or not?

The Advisory track current market conditions so buyers and sellers can gain an independent view of how easy it would be to buy and sell their home in their area. This makes it easier for good agents that are honest about market conditions to value and manage expectations. For example, in BH17 (Poole) 88% of the properties on the market are under offer and M2 in Manchester is one of the worst performers according to this index, showing that ‘average property prices’ can mislead buyers and sellers.

From PropCast’s perspective, the hot markets at postcode level don’t necessarily track the overall increases and decreases seen even at town and city levels, with Poole, Bristol and Liverpool having some of the busiest markets, and Manchester, Birmingham and London having some of the slower ones.

To find out what’s happening in your postcode visit the House Selling Weather Forecast at https://www.theadvisory.co.uk/propcast/