LATEST: Interest rate rise today ‘almost certain’ as inflation sticks at 8.7%

The rate of price rises has remained stuck at 8.7% despite a slight decrease expected by economists which would have gone some way to buoy the jittery housing market.

Worrying figures from the Office of National Statistics today sent a stark warning to households with grim news on consumer prices indicating that fixed mortgage rates could still rise even higher making it harder to remortgage or buy a home.

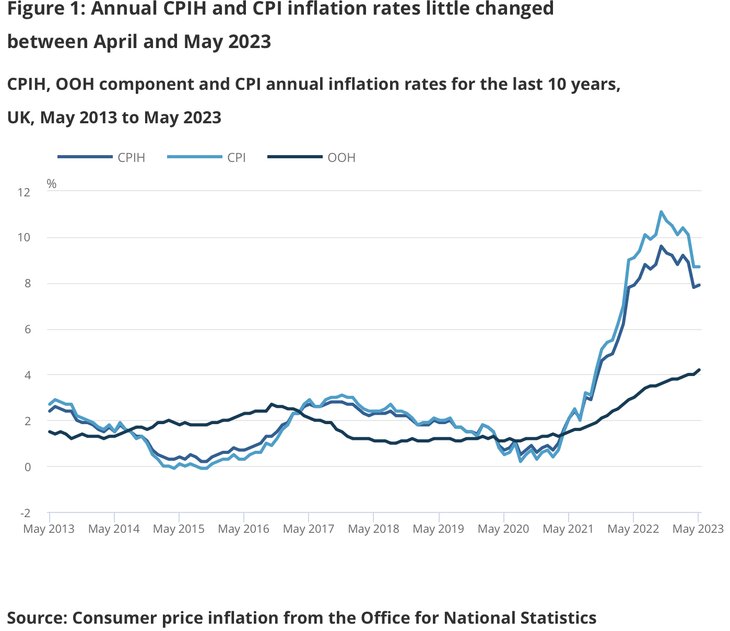

The Office for National Statistics (ONS) said this morning that the rate of price rises has remained at 8.7% in the year up to May, the same as the rate in April, despite expectations of a fall.

Measures of inflation and prices include consumer price inflation, producer price inflation and the House Price Index and the data is used by the Bank of England to help set interest rates.

A slight decrease to 8.4% had been expected by economists which would have gone some way to calm the mortgage fears of thousands, particularly as the BoE is due to decide on whether to raise interest rates tomorrow.

RISING PRICES

Falling fuel prices have been offset by rising prices for air travel, recreational and cultural goods and services and second-hand cars.

Core inflation — that strips out food, energy, alcohol and tobacco — rose to 7.1%, from 6.8%.

Prices for food and non-alcoholic beverages eased further from its March high of 19.2% 18.4%.

Prices for food and non-alcoholic beverages eased further from its March high of 19.2% 18.4%.

Inflation had been on course to ease as the annual measure of price growth no longer included the jump in energy prices.

Inflation began to increase in late 2021, when problems linked to COVID lockdowns and the associated worker shortages meant demand for goods could not be met.

REACTION

Tom Bill, head of UK residential research at Knight Frank, says: “Over the last two months, inflation has replaced the mini-Budget as the biggest obstacle facing the UK housing market.

“Rising interest rate expectations have pushed up monthly mortgage payments, which will contribute to a slowdown in trading activity and house prices this year.

“That said, the wage growth driving core inflation higher is one of the reasons we don’t expect a steep double-digit fall in house prices this year.

“Record levels of housing equity, the availability of longer mortgage terms and the popularity of fixed-rate products in recent years should also prevent a collective cliff-edge moment for the housing market.”

Disaster

Lewis Shaw, founder of Mansfield-based Shaw Financial Services, says: “This is a disaster. With CPI having stayed the same and core CPI rising, we can expect to see gilt yields spike as investors look for higher returns from government debt.

“This spells terrible news for the property market because the Bank of England will be under enormous pressure to hike rates tomorrow, almost certainly by 50 basis points.

“The knock-on effect is mortgage rates will continue to soar and the pain for households will intensify. With mortgage rates already at the most painful level since the 90s, we can expect a slowdown in the property market and house prices are well and truly in the crosshairs.”

It almost certainly signals an impending increase in the base rate tomorrow.”

Riz Malik, director of Southend-on-Sea-based independent mortgage broker, R3 Mortgages, says: “The persistent 8.7% CPI inflation, coupled with rising core inflation, was certainly not the news we hoped for.

“It almost certainly signals an impending increase in the base rate tomorrow.

“Our hope is that the Bank of England will restrict its actions to a modest hike, preferably no more than 25 basis points given this data. This is not the data the mortgage market needs.”

A further Bank rate rise is a nailed-on certainty.”

And Andrew Montlake, managing director of the UK-wide mortgage broker, Coreco, says: “The latest inflation data is set to upset an awful lot of people, leading to a new set of rates rises that will compound the pain of a cost of living crisis on the public.

“A further rise in Bank of England base rate is a nailed-on certainty, and there is now a real possibility they could panic and increase by a further 0.5% straight to 5%.

“The Bank has one job to do and it is painfully clear that the tool they are currently using is a blunted instrument against inflation that is now endemic.

“Rather than keep doing the same thing, they should pause for thought and look at a different approach before they inflict real harm on the economy and on people’s livelihoods.”

The bank of England is using tactics from the 1970’s and 1980’s trying to fix a global issue by playing with local factors. Its like trying to stop a burst dam by turning off the water in the village. Absolutely no affect and can be explained by poor education in UK economics.

Cause and effect needs to be considered carefully. Not running around increasing rates like a bull in a crypto shop., An increase in mortgage rates and inflation has caused the now huge self employed sector to give themselves pay rises. Also leaving the EU has had a massive effect on lack of staff which has increased wages for unproductive staff affecting UK plc as tourists realize we don’t have customer service. This has also caused rents to rise as many landlords sold up and continue to sell to not pay these interest rates and also because government took away tax relief for a legitimate business expense.

Most of the current inflation causation is external to the UK so high rates of interest only accelerates price rises across energy and food sectors mostly.

They need to focus on food and energy and come up with a plan to fix these areas and the rest will follow.

I cant believe the incompetence at this level. This will impact on how our universities are viewed because it shows that they have no real world of work knowledge. They just blag their way through life using verbosity and ineffective algorithms. And actually just crossing their fingers.

Bring back Mark Carney asap.

I’m convinced that the Bank of England actually have no clue what they are doing. Raising interest rates is designed to reduce money in the consumers pocket. It also increases money in savers pocket. The only way it reduces money is by increasing mortgage payments and as most people are on fixed rates, the increases that they have made over the last 13 months will take some time to work into the system. if they continue to increase then when these increases actually hit peoples pocket, it will hurt so much that we could have a very serious problem. I just don’t understand how the Bank of England can’t see this or perhaps they have another agenda and are using inflation as an excuse!!